As an economic storm looms over the Netherlands, the government is working on a modest stimulus package. It’s doing everything it can to avoid disrupting the budget too much. But what’s really needed are major interventions. The government is growing too fast, living beyond its means, and investing too little.

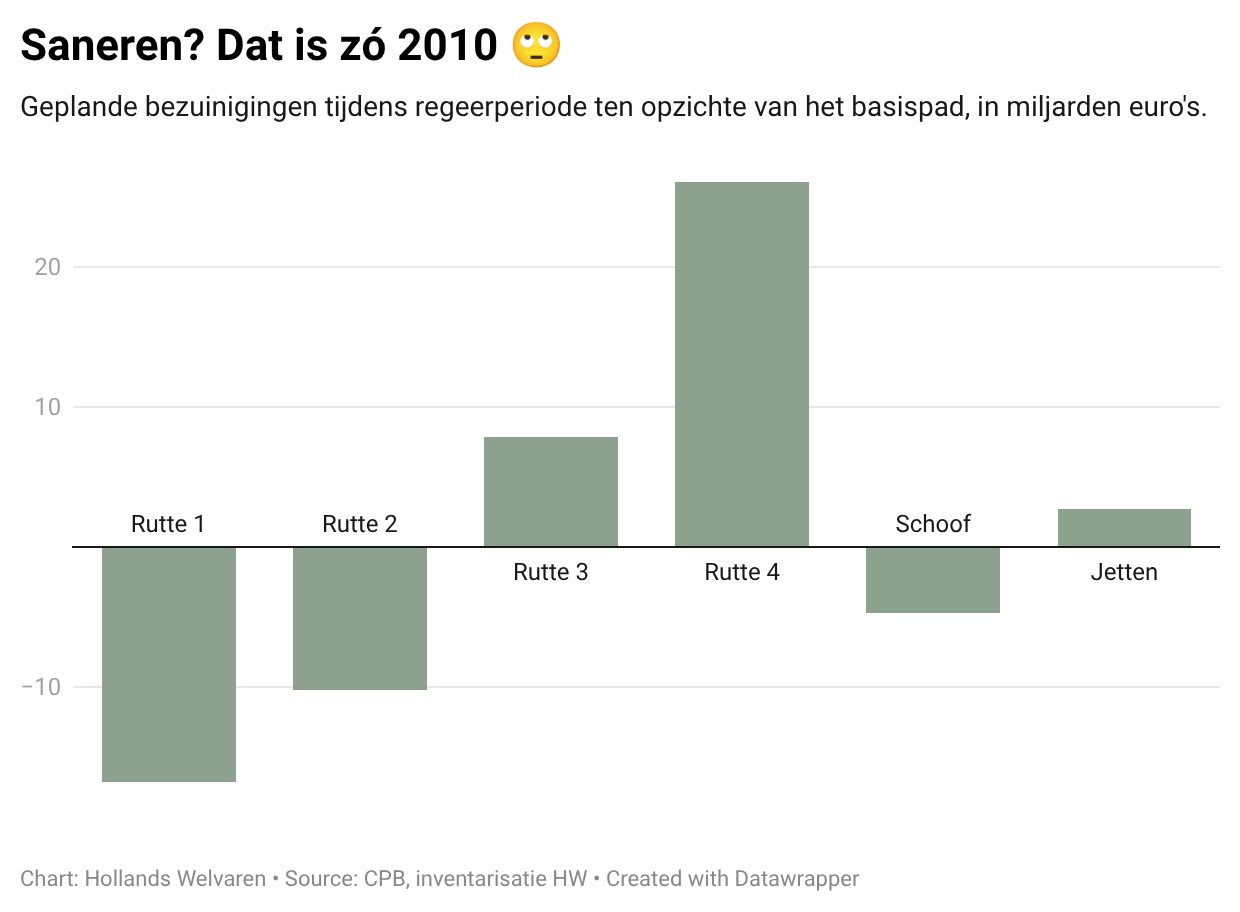

A 12-billion-euro austerity package. Of course, it’s not pleasant for an opposition party to agree to this, but Jesse Klaver is doing it anyway; after all, the country must be governed, even if the cabinet lacks a majority. Behind the scenes, Eelco Heinen has been helping to work out the details: naturally, the package needs to be somewhat balanced in order to secure a majority in Parliament. The retirement age will rise faster, as will the healthcare deductible. Citizens and businesses will pay more in taxes. Healthcare will become more austere, the economy will become greener, and civil servants will face the axe.

Is that never going to happen? It already has.

In 2012, Geert Wilders withdrew his support for Rutte’s first cabinet in the midst of the euro crisis. The opposition parties GroenLinks, D66, and ChristenUnie helped the cabinet secure a majority for significant spending cuts and tax increases through the Spring Agreement (also known as the Kunduz Agreement). Jesse Klaver had been in the House for less than two years, and Heinen had just begun his rise as the VVD’s financial conscience, serving as financial policy advisor to the VVD parliamentary group.

Both politicians have since gone on to have impressive careers and made their mark on The Hague. Klaver is now the party leader of the largest opposition party, Progressive Netherlands. Heinen serves as Minister of Finance. Yet they have never been able to repeat their 2012 feat.

Later in 2012, the VVD and PvdA signed another coalition agreement that called for even deeper spending cuts. But since then, it seems that no one in The Hague wants to be seen with an axe—or a chainsaw —anymore. Since then, coalition agreements have mainly been about spending even more money.

Are these budget cuts really necessary?

How bad is that? Maybe there’s simply no need to cut spending right now. At 45% of the economy, isn’t the national debt still well below the European limit of 60%?

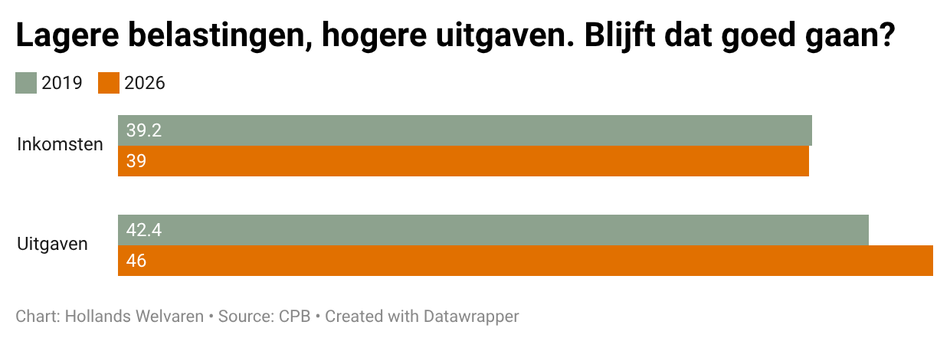

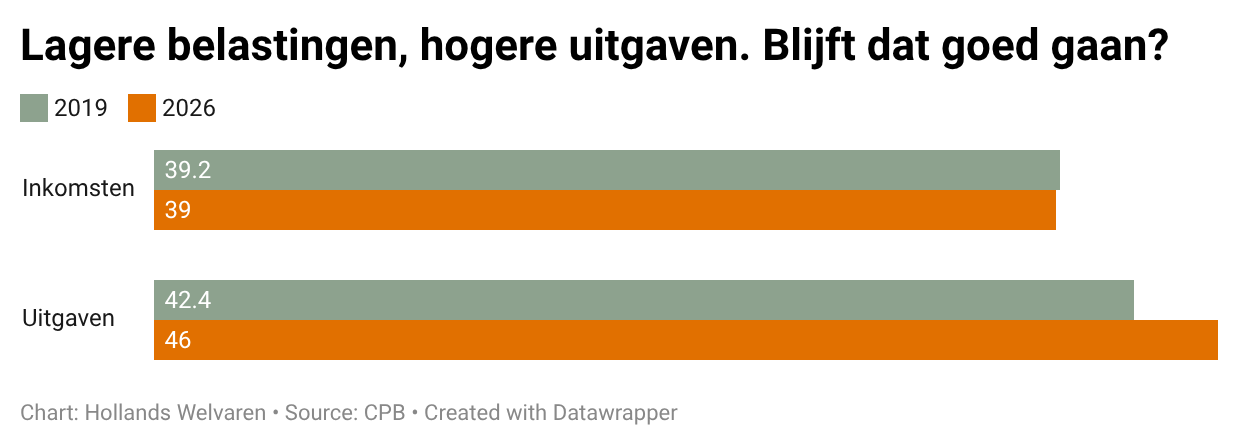

But anyone who looks at how taxes and government spending have evolved since the COVID-19 crisis can see how the situation has spiraled out of control. In 2019, the last “normal” year, tax revenues still accounted for 39.2% of our economy. Now that figure is slightly lower.

So has government spending gone down? No, on the contrary, it has risen sharply, to 46% of the economy.

Fortunately, the government receives more revenue than just from taxes. Consider natural gas revenues and dividends from state-owned companies (such as De Nederlandsche Bank, Holland Casino, and TenneT). As a result, the Netherlands still had a budget surplus in 2019. But here, too, the outlook for the treasury has become less rosy. 'Groningen' is being filled with concrete, TenneT actually had to borrow money from the government to invest in the power grid, and DNB slipped into the red. As a result, these 'non-tax revenues' are also declining—while government spending continues to rise unabated.

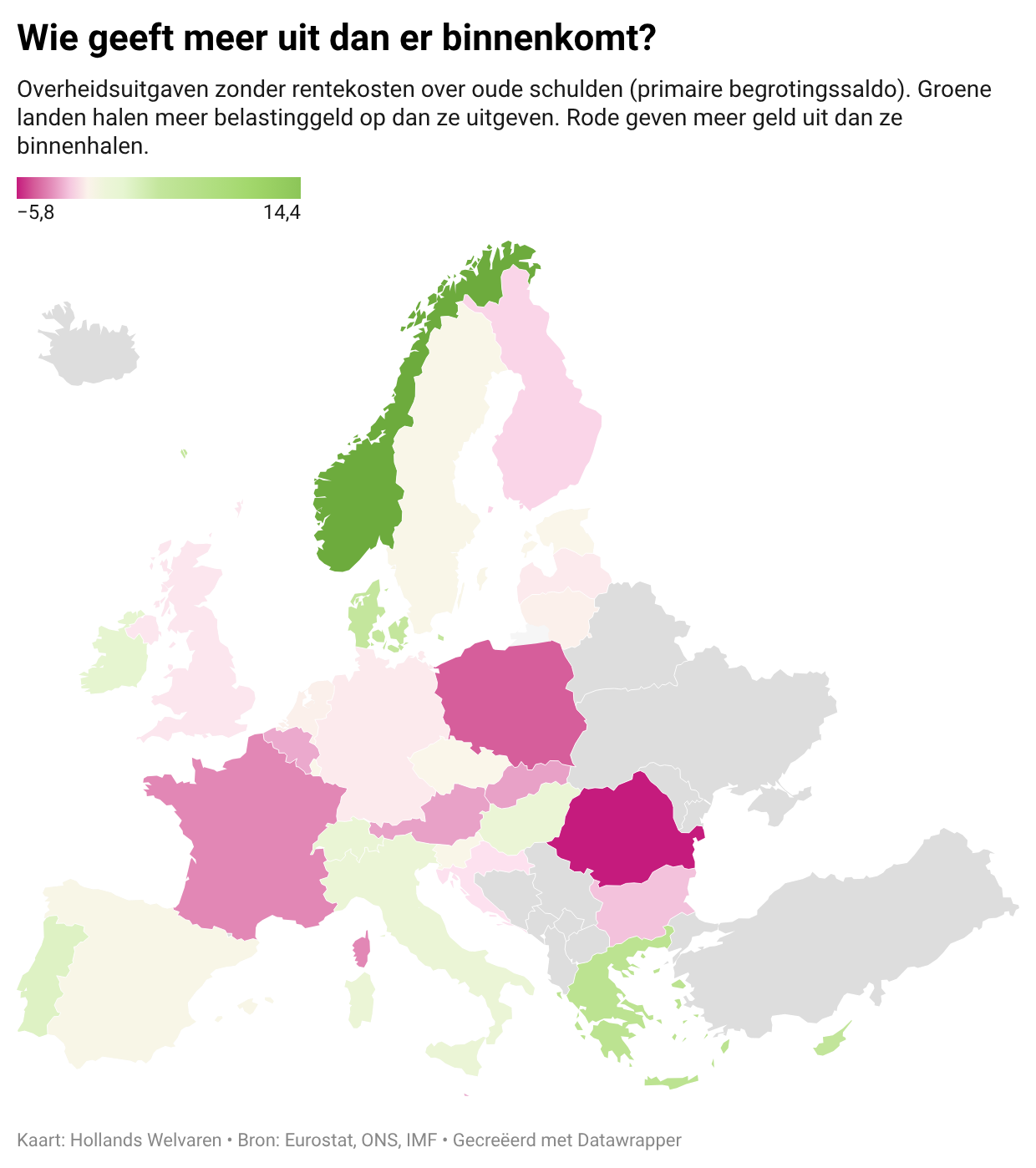

None of this is inevitable. It’s a specifically Dutch laxity. If you look at other small, wealthy European countries, they do manage their money wisely. The map below shows the so-called primary budget balance of European countries. This represents all government spending minus interest expenses. This allows you to see whether current spending can be covered by current revenue and filters out interest expenses resulting from wasteful previous generations (as is the case for Italy).

With a deficit of -0.9%, the Netherlands is performing slightly better than Germany (-1.2%) or the UK (-1.4%). And certainly better than France (-3.4%) and Belgium (-2.8%). But it is doing much worse than the Southern countries we looked down on so much during the euro crisis. They have, however, managed to turn things around since then.

Perhaps even more importantly, the Netherlands is also performing much worse than Switzerland, Denmark, and Ireland—a group of small, wealthy European countries that we really ought to be part of.

Investing in the future? Why should we?

This article is for paid members only

To continue reading this article, upgrade your account to get full access.

Subscribe NowAlready have an account? Sign In